Tutorial 1: Univariate

hhh4()

Using weekly counts of norovirus gastroenteritis from Berlin

Template: univariate.R

Abstract

This tutorial introduces endemic-epidemic models using a single time

series of counts. Univariate analyses are not the main target of

hhh4() and many other tools exist for this simple case, but

it can serve as an accessible first encounter of the modelling concept.

We use data on weekly counts of norovirus infections in Berlin, Germany,

readily provided as an "sts" object for use with the

surveillance package. If you wish to learn more about

this specific data class and available methods, see the "sts" tutorial. The same dataset is

also used in the multivariate tutorial,

but then disaggregated by district.

Some initial code is provided in the R script template

univariate.R that is part of the tutorials.zip

archive, as are the necessary data files.

Data

We use data from routine surveillance in Germany carried out by Robert Koch Institute. We have

already prepared these as "sts" (surveillance time

series) data, which you can directly load from the provided RData file.

Lade nötiges Paket: spLade nötiges Paket: xtableThis is surveillance 1.23.1; see 'package?surveillance' or

https://surveillance.R-Forge.R-project.org/ for an overview.Loading objects:

noroBE

rotaBEWe focus on noroBE, which contains weekly counts of

confirmed cases of norovirus

gastroenteritis in Berlin, 2011–2017, stratified by district. These

data have already been used as an example in at least two publications

on hhh4 extensions (for serial interval

distributions and social contact

data, respectively).

The rotaBE dataset contains the same for rotavirus

gastroenteritis, which you can explore if you want to play around a

bit more.

In this tutorial, we only look at the overall time series aggregated over all districts:

-- An object of class sts --

freq: 52

start: 2011 1

dim(observed): 364 1

Head of observed:

overall

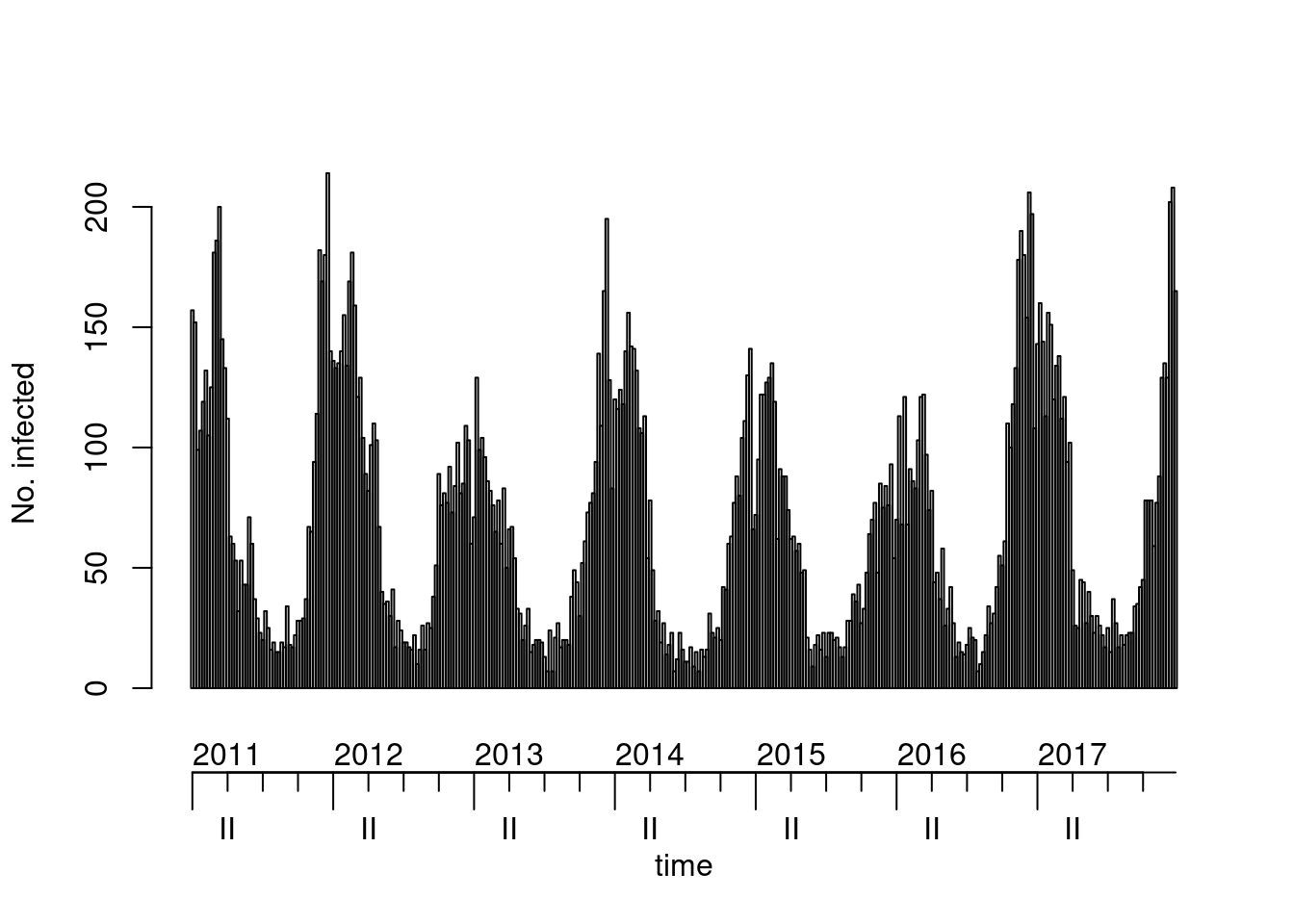

[1,] 157Task

Look at a plot() of the data. You can also try a

ggplot2 version via ggplot2::autoplot(),

or plot an as.ts() or xts::as.xts() (if you

have that) version of the data.

Alternatively, convert the "sts" object to a “tidy” data

frame via tidy.sts() and use your favourite plotting

tool.

Solution

## alternative visualizations (and there are probably more)

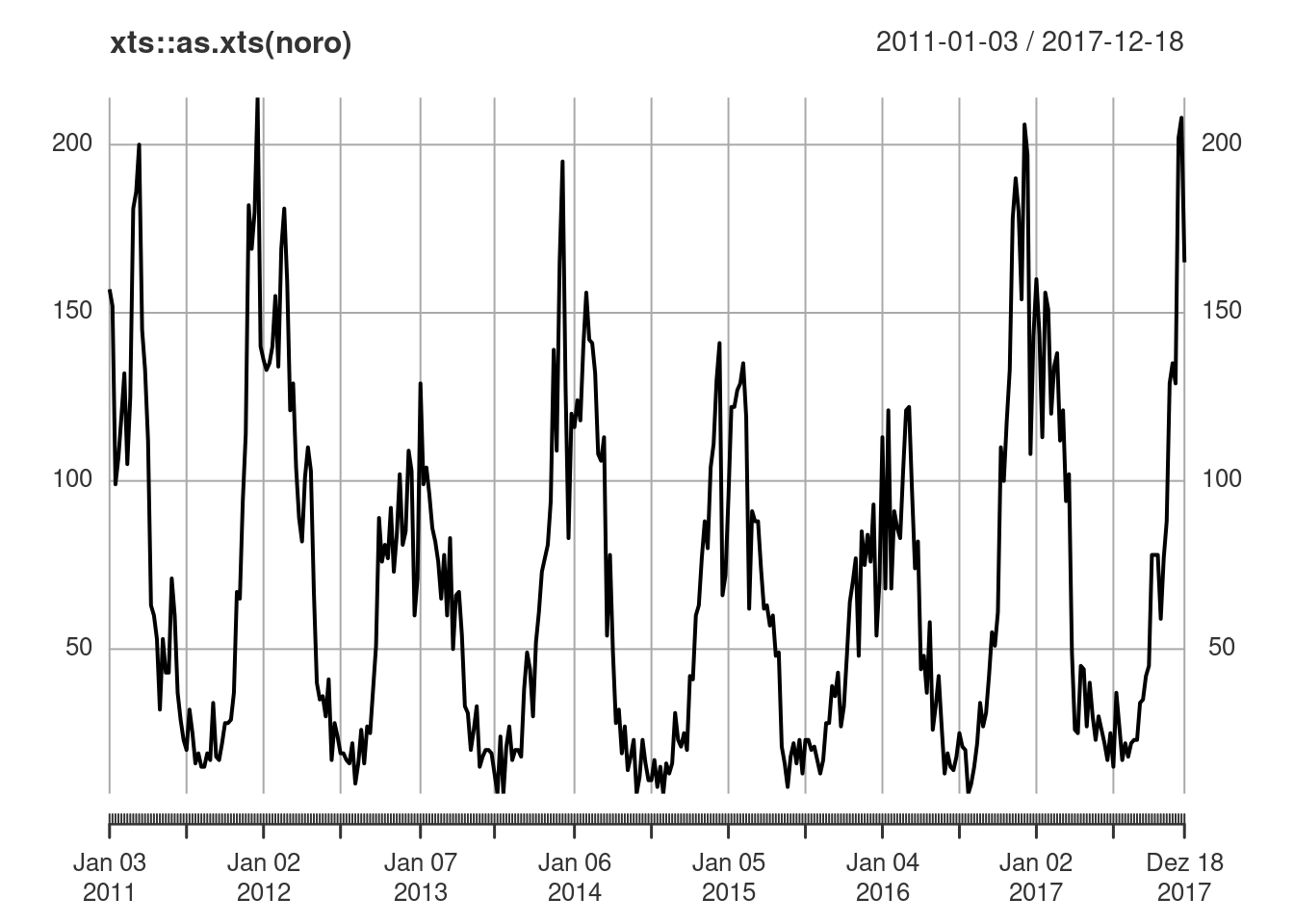

plot(noro, col = 8, epochsAsDate = TRUE) # alternative colour & time axis setup

## there is a clear yearly seasonality, see also

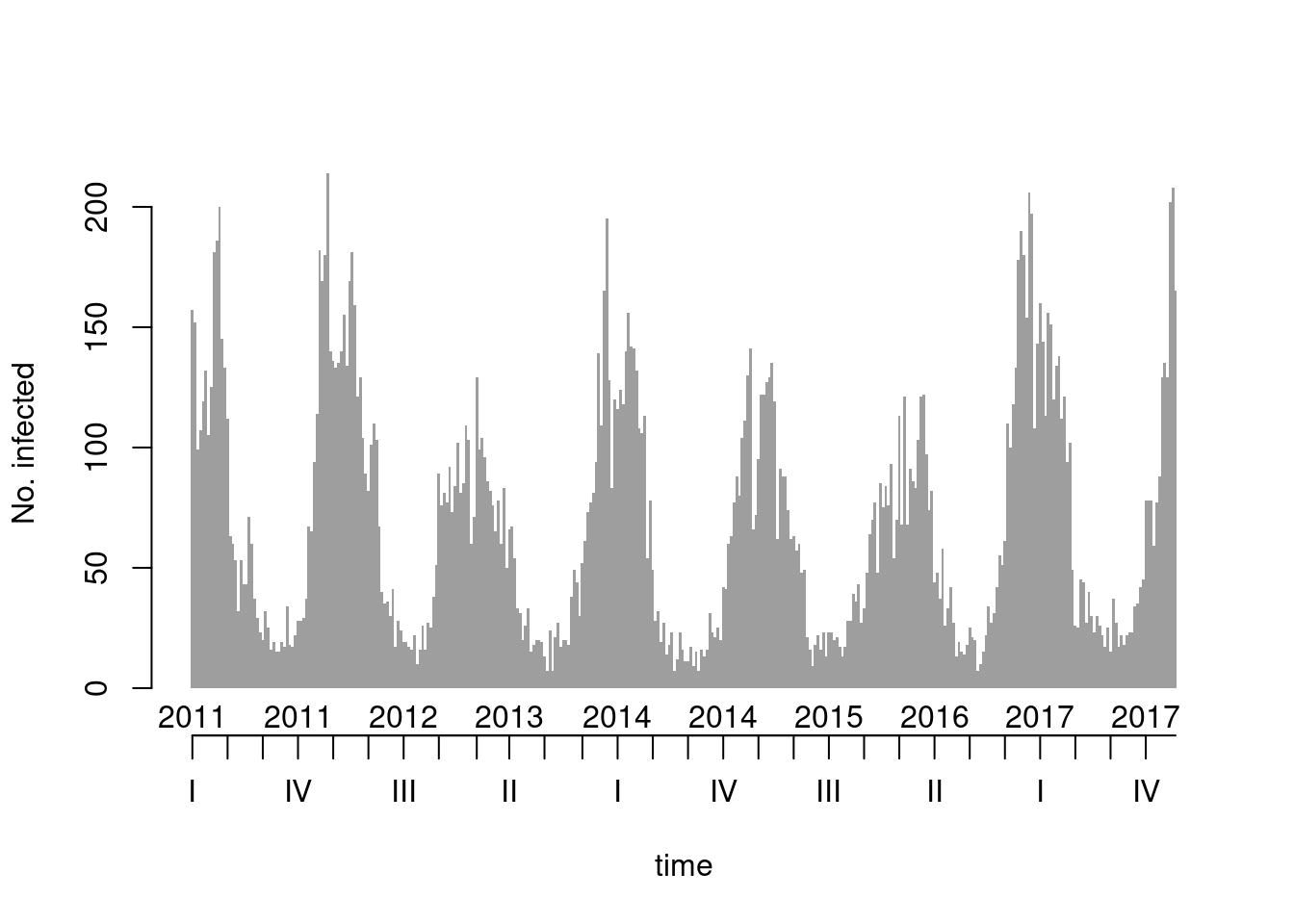

## the basic "ts" monthplot()

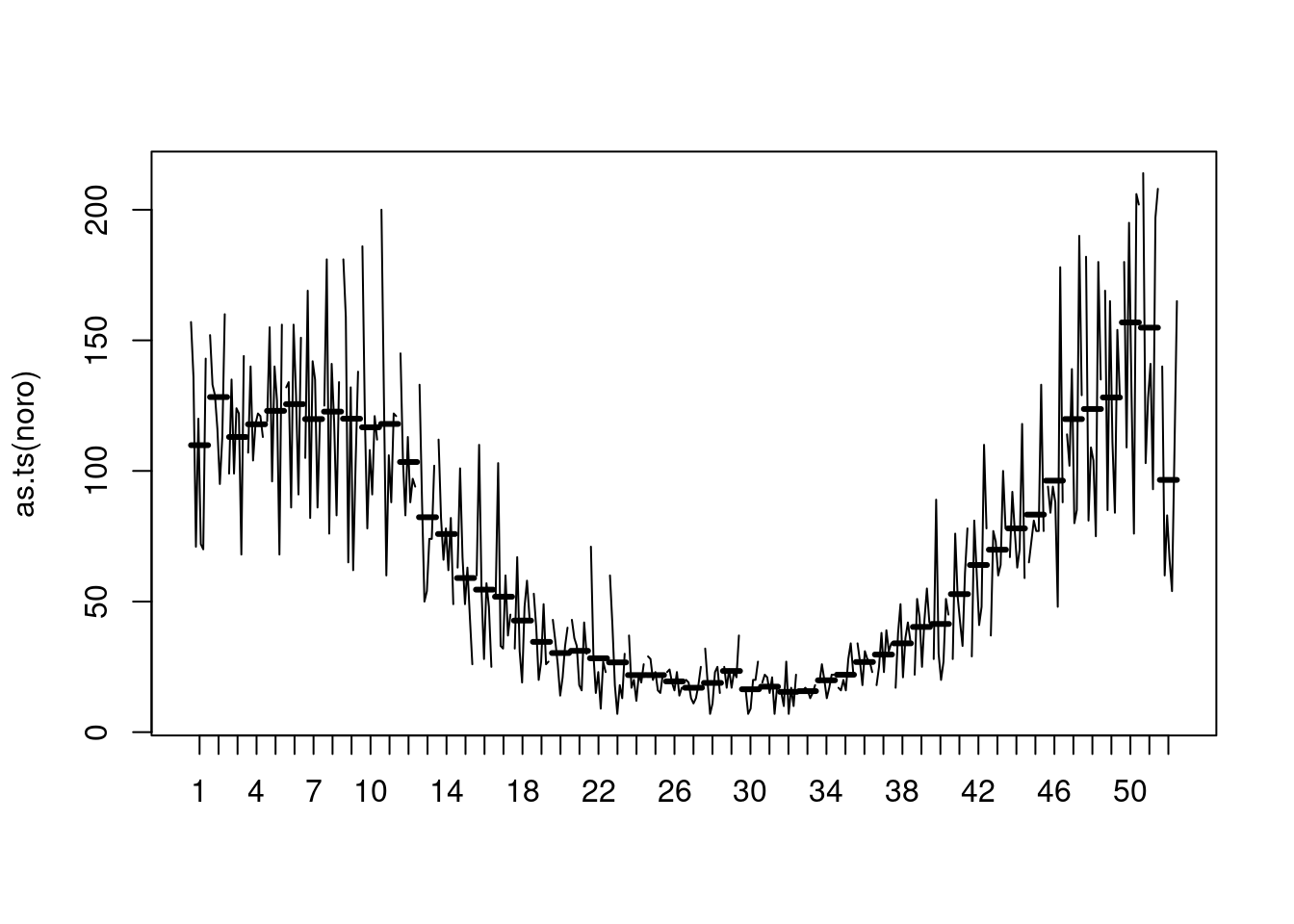

as.ts(noro) |> monthplot(lwd.base = 3)

## => (unfortunate) peak around Christmas, minimum around calendar week 32

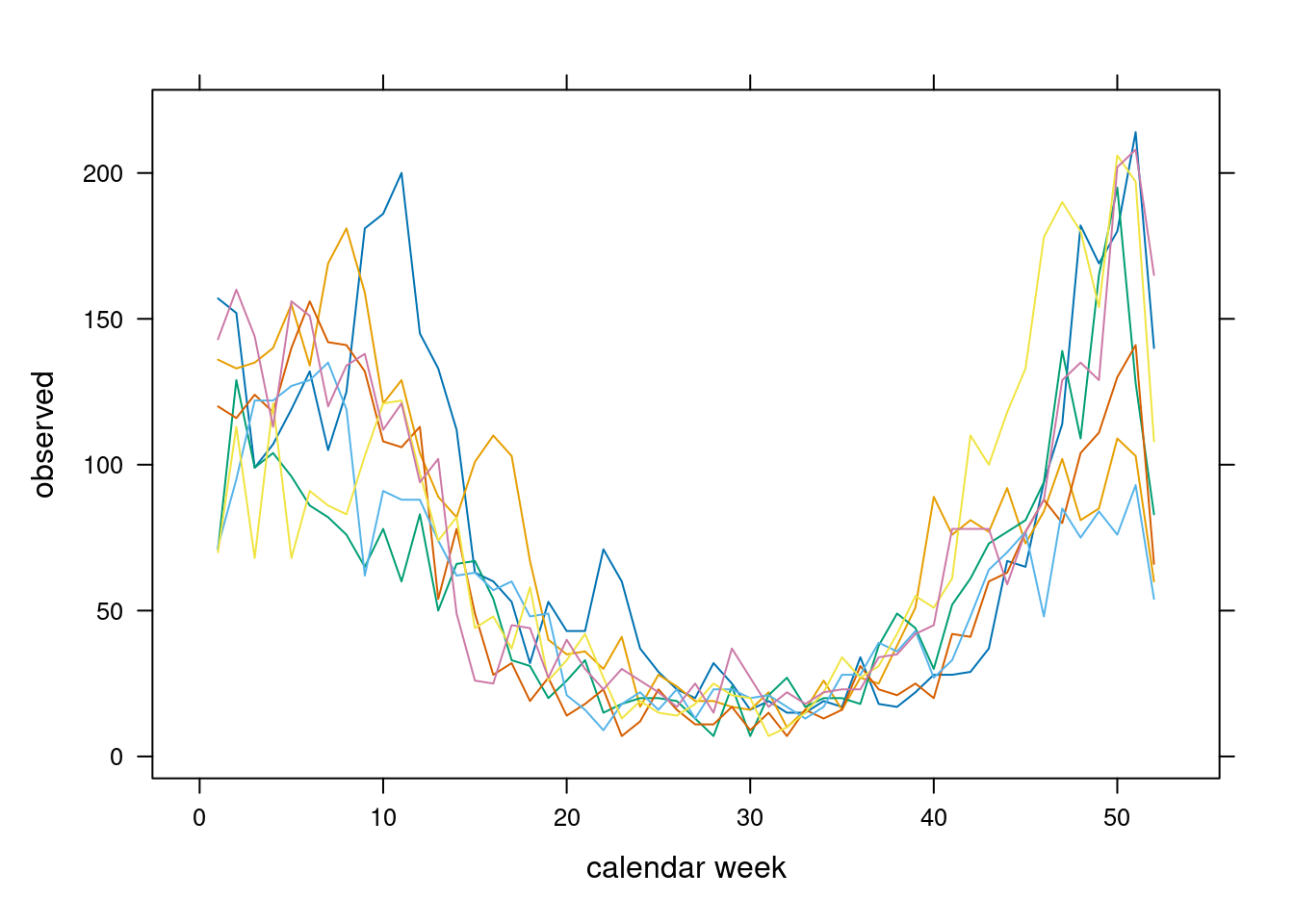

## or use, e.g., lattice::xyplot() with the "tidy" dataset

lattice::xyplot(observed ~ epochInYear, data = tidy.sts(noro),

groups = year, type = "l", xlab = "calendar week")

Fitting hhh4() models

We don’t have any exogenous covariates in this example, but we can at least capture seasonality by including transformations of time (pairs of sine-cosine terms) as covariates in the model.

In statistical terms, we will fit simple models of the form

\[ Y_t | Y_{t-1} \sim \operatorname{NegBin}(\nu_t + \lambda_t y_{t-1}, \phi) \]

where the log-linear predictors \(\nu_t\) (endemic component)

and \(\lambda_t\) (ar

component) could use regression formulae of the form

\[ \alpha + \sum_{s=1}^S \left\{ \gamma_s \sin(s \omega t) + \delta_s \cos(s \omega t) \right\} \]

with S harmonics of “fundamental frequency” \(\omega=2\pi/52\).

Such a formula for use in hhh4() model

components can be created very easily, here adding just one harmonic to

an intercept-only formula:

~1 + sin(2 * pi * t/52) + cos(2 * pi * t/52)The basic syntax for fitting an endemic-epidemic time-series model is

where the first argument gives the data as an "sts"

object (here: noro) and the second argument specifies the

model in the form of a list. For example, the rudimentary intercept-only

model NegBin\((\nu + \lambda y_{t-1},

\phi)\) could be specified using the following control list:

Task

Estimate a few different hhh4() models with seasonality

(e.g., using f = f1 from above) and compare them using

AIC(fit1, fit2, ....) (Akaike Information

Criterion, smaller is better).

Note that you can update() a previously fitted model and

only specify what you would like to change. For example, if

fit was the intercept-only model from above, you could

estimate a new model where the autoregressive component uses the

f1 formula as follows:

Solution

## try an endemic-only model with one harmonic

fit_endemic <- hhh4(noro, list(end = list(f = f1), family = "NegBin1"))

## try the intercept-only endemic-epidemic model

fit00 <- hhh4(noro, list(ar = list(f = ~1), end = list(f = ~1), family = "NegBin1"))

## try various options with seasonality

fit01 <- update(fit00, S = list(ar = 0, end = 1)) # constant lambda

fit10 <- update(fit00, S = list(ar = 1, end = 0)) # constant nu

fit11 <- update(fit00, S = list(ar = 1, end = 1)) # both seasonal

AIC(fit_endemic, fit00, fit01, fit10, fit11) df AIC

fit_endemic 4 3151.523

fit00 3 3057.533

fit01 5 2969.641

fit10 5 2991.624

fit11 7 2966.411Inspecting the fit

The list of methods(class = "hhh4") is quite long. Some

useful ones for inspecting model fits are summary(),

plot() (see ?plot.hhh4), pit(),

and residuals().

Task

Inspect some of the fitted models.

Solution

Call:

hhh4(stsObj = object$stsObj, control = control)

Coefficients:

Estimate Std. Error

ar.1 -0.481167 0.065909

end.1 3.010150 0.102923

end.sin(2 * pi * t/52) 0.032159 0.058467

end.cos(2 * pi * t/52) 1.010425 0.049928

overdisp 0.051619 0.005481

Log-likelihood: -1479.82

AIC: 2969.64

BIC: 2989.11

Number of units: 1

Number of time points: 363 ## transform sine-cosine coefficients to amplitude-shift parameters,

## exp-transform the intercepts to get to the response scale,

## and show the dominant eigenvalue ("=" epidemic proportion)

summary(fit01, amplitudeShift = TRUE, idx2Exp = TRUE, maxEV = TRUE)

Call:

hhh4(stsObj = object$stsObj, control = control)

Coefficients:

Estimate Std. Error

exp(ar.1) 0.618062 0.040736

exp(end.1) 20.290441 2.088360

end.A(2 * pi * t/52) 1.010937 0.051310

end.s(2 * pi * t/52) 1.538980 0.031096

overdisp 0.051619 0.005481

Epidemic dominant eigenvalue: 0.62

Log-likelihood: -1479.82

AIC: 2969.64

BIC: 2989.11

Number of units: 1

Number of time points: 363 ## epidemic proportion of disease incidence is estimated to be 62%

## the rest isn't necessarily non-epidemic, but imported/unexplained

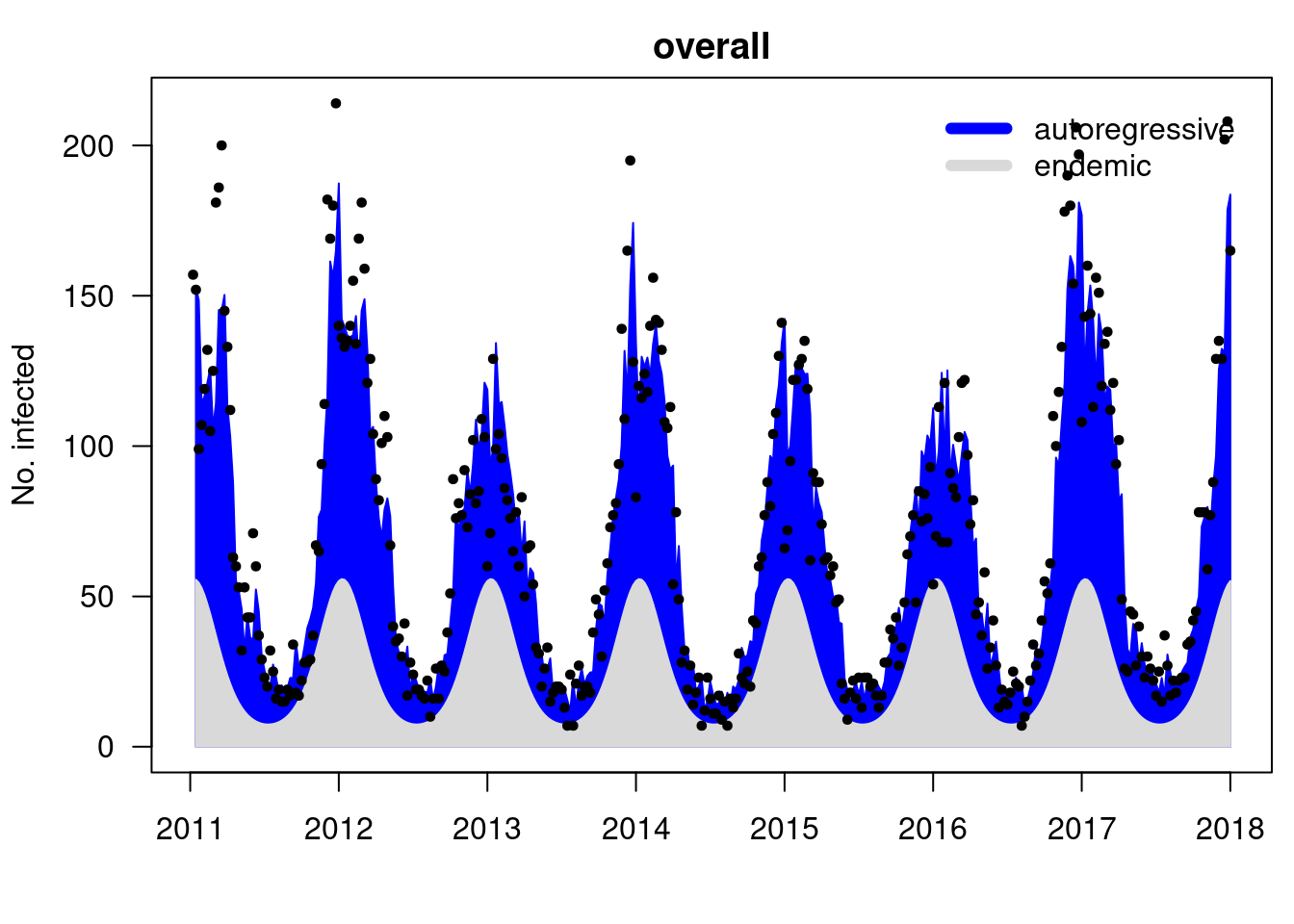

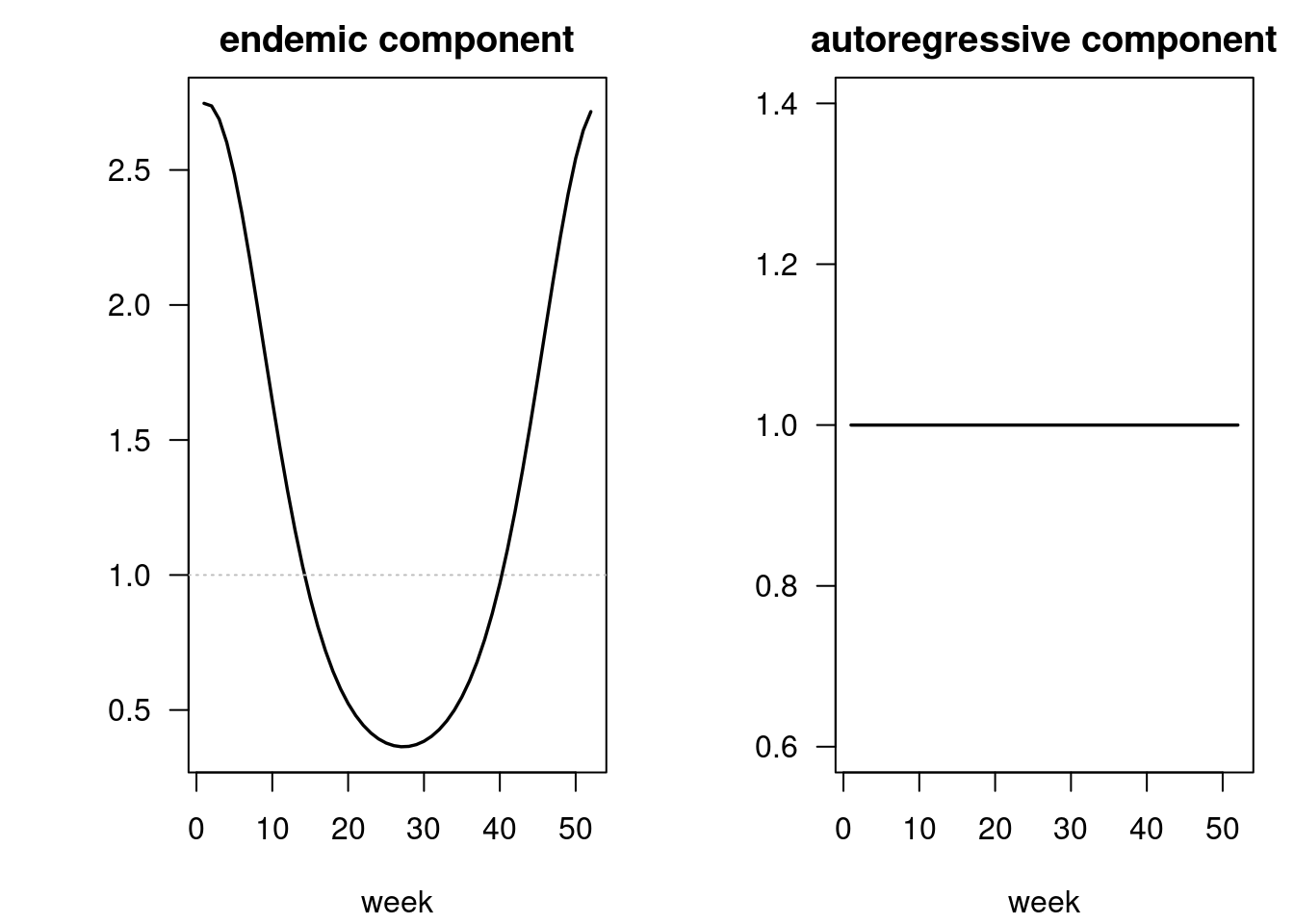

## show the fitted model components

plot(fit01) -> .components

List of 1

$ overall: num [1:363, 1:8] 153 148 114 117 121 ...

..- attr(*, "dimnames")=List of 2

.. ..$ : NULL

.. ..$ : chr [1:8] "mean" "epidemic" "endemic" "epi.own" ...[1] 0.6210123

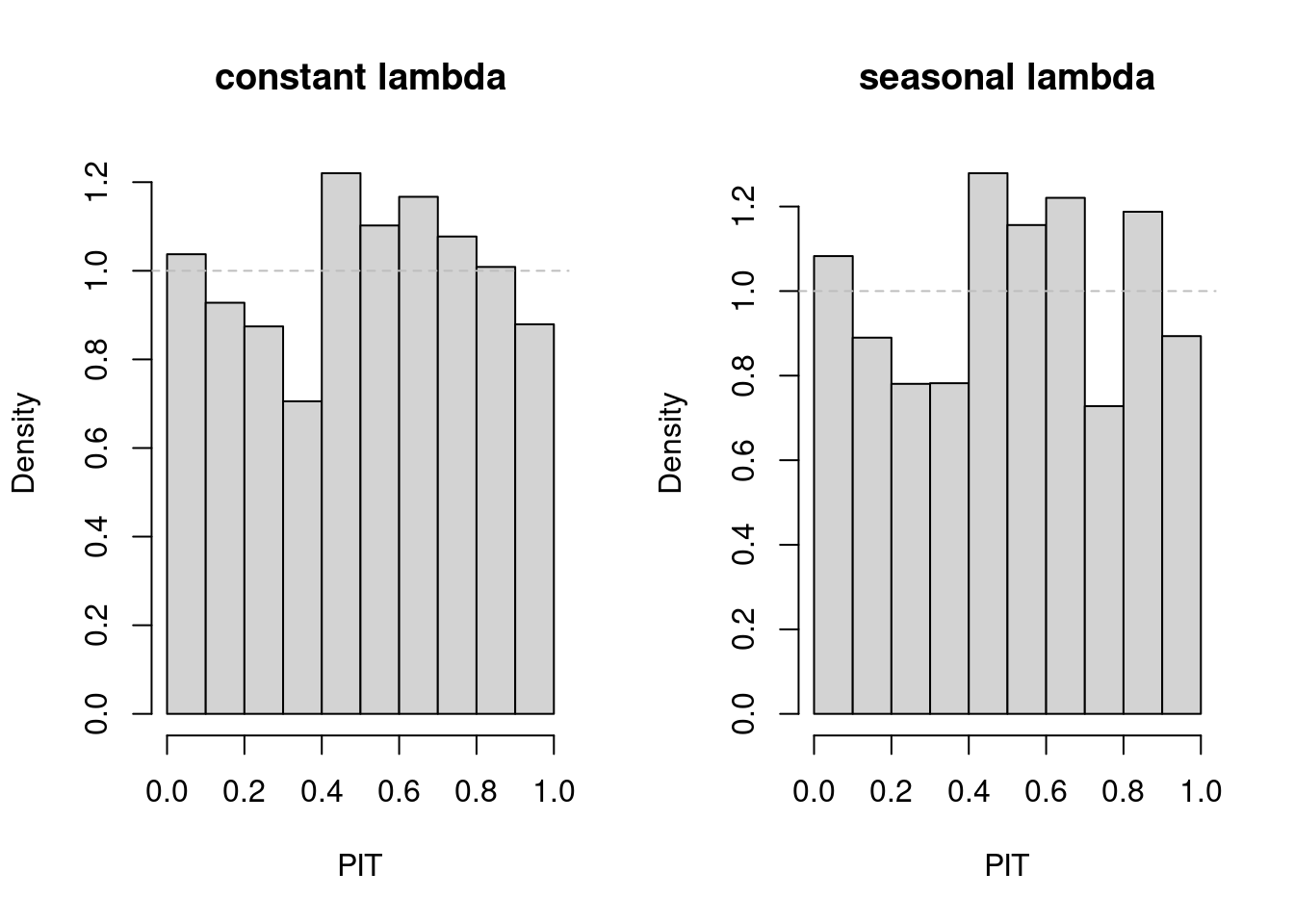

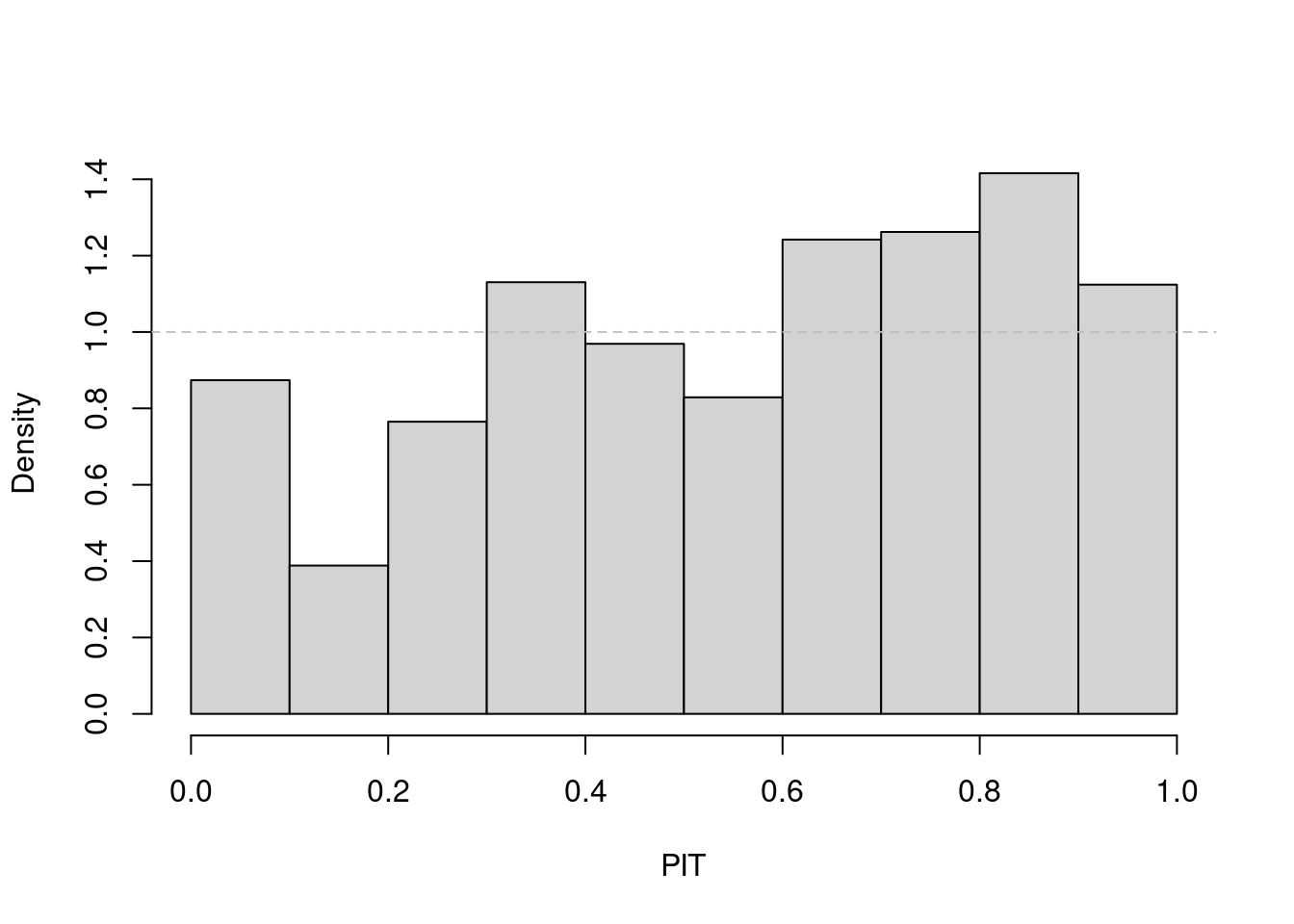

## PIT plot to check model calibration

opar <- par(mfrow = c(1,2))

pit(fit01); title(main = "constant lambda")

pit(fit11); title(main = "seasonal lambda")

par(opar)

## no clear preference

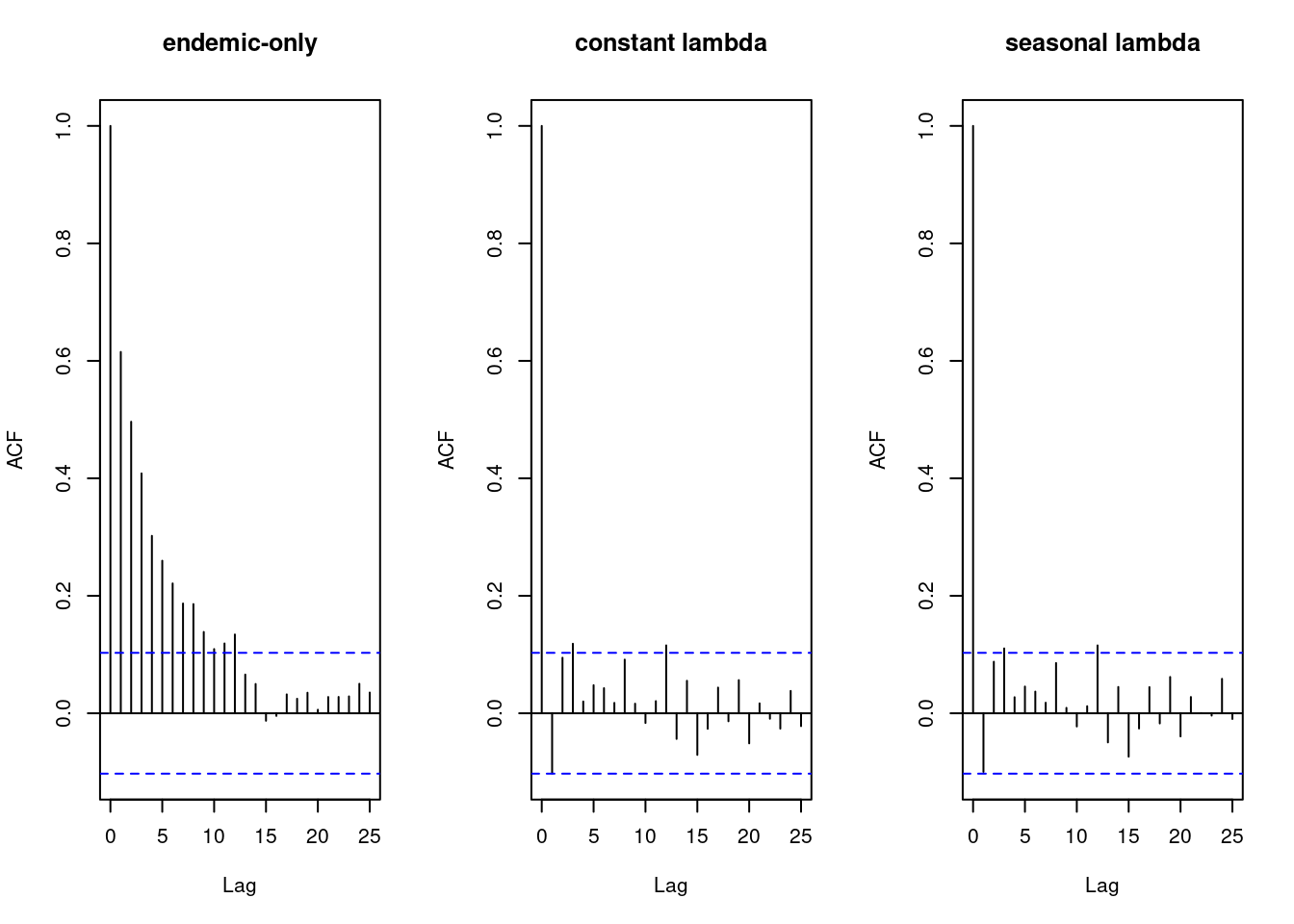

## check residual correlation

opar <- par(mfrow = c(1,3))

acf(residuals(fit_endemic), main = "endemic-only") # strong residual correlation

acf(residuals(fit01), main = "constant lambda")

acf(residuals(fit11), main = "seasonal lambda")

Forecasting

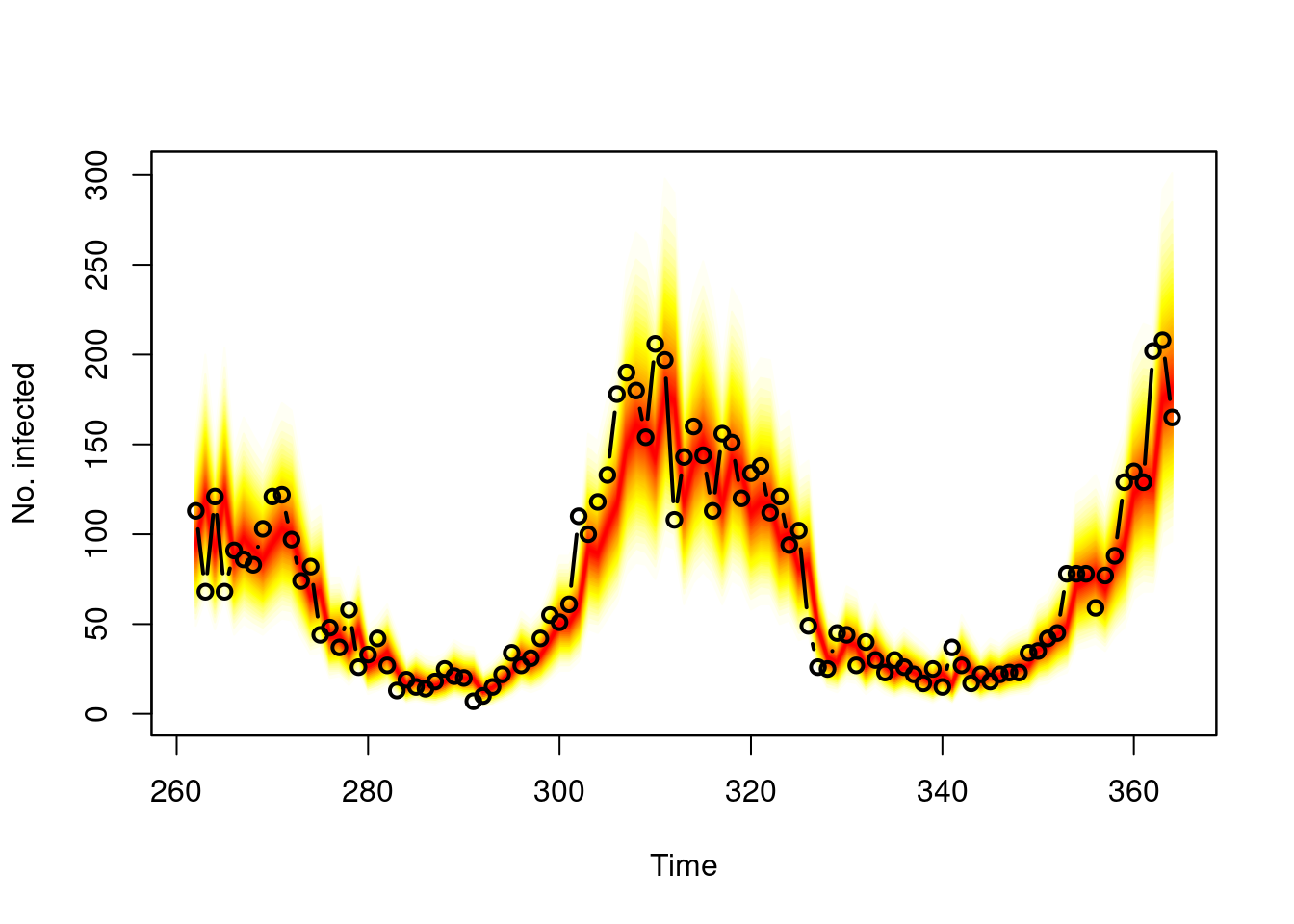

Task

Use oneStepAhead() to produce “rolling” weekly

forecasts, e.g., over the last two years, and plot() the

result. You should also look at a pit() histogram of these

probabilistic forecasts.

Solution

## compute "rolling" weekly forecasts starting from 2016

startidx <- match(2016, year(noro))

osa01 <- oneStepAhead(fit01, startidx, verbose = FALSE)

plot(osa01)

2.5 % 10.0 % 50.0 % 90.0 % 97.5 %

262 55 67 94 127 147

263 71 86 120 161 186

264 53 64 91 123 142

265 71 87 122 164 189

266 50 61 87 118 137

267 56 69 98 132 153

## forecast from fit11 and compare mean scores() (where smaller is better)

osa11 <- oneStepAhead(fit11, startidx, verbose = FALSE)

rbind("constant lambda" = colMeans(scores(osa01)),

"seasonal lambda" = colMeans(scores(osa11))) logs rps dss ses

constant lambda 4.169023 10.59943 6.514457 455.2519

seasonal lambda 4.167993 10.56779 6.517539 457.9010